FOR Communication 4/2024: What's wrong with the Polish tax system?

The tax system has a profound impact on a country's economic growth for two reasons. Firstly, in developed countries, taxes typically amount to the equivalent of one-third to even half of the GDP. Such high level of taxation obviously affects taxpayers’ economic activity. Secondly, for the state to collect taxes, it must maintain appropriate regulations defining the tax base (what to tax) and rates (how much—as a percentage or as an amount—must be paid from a given base). These regulations influence decisions regarding, for example, the form of contracts between individuals, the legal form of business activities, or how savings are invested. Moreover, the complexity and variability of the rules generate additional uncertainty for payers concerning whether they must pay a tax at all, and if so, at what rate, as well as whether their situation might change in the near or distant future.

The overall level of taxes (taxation in relation to GDP) depends primarily on the size of government spending—although states also derive income from other sources, such as owned assets, and incur debt to cover deficits. It is not possible in a market economy to finance all public expenditures this way, which often reaches 50% of GDP. Without addressing the expenditure side, it is therefore impossible to reduce the overall level of taxation.

However, tax regulations can be changed without reforming expenditures. A well-designed tax system allows taxpayers to easily calculate and pay their dues and provides funds to finance public expenditures. Conversely, a poorly designed tax system is a burden on taxpayers and discourages them from productive activities, such as working and investing.

What negatively distinguishes Poland from other countries is not so much the level of taxes, although it has significantly increased in recent years and is higher than the OECD average, but the lack of neutrality, the complexity, and variability of the system.

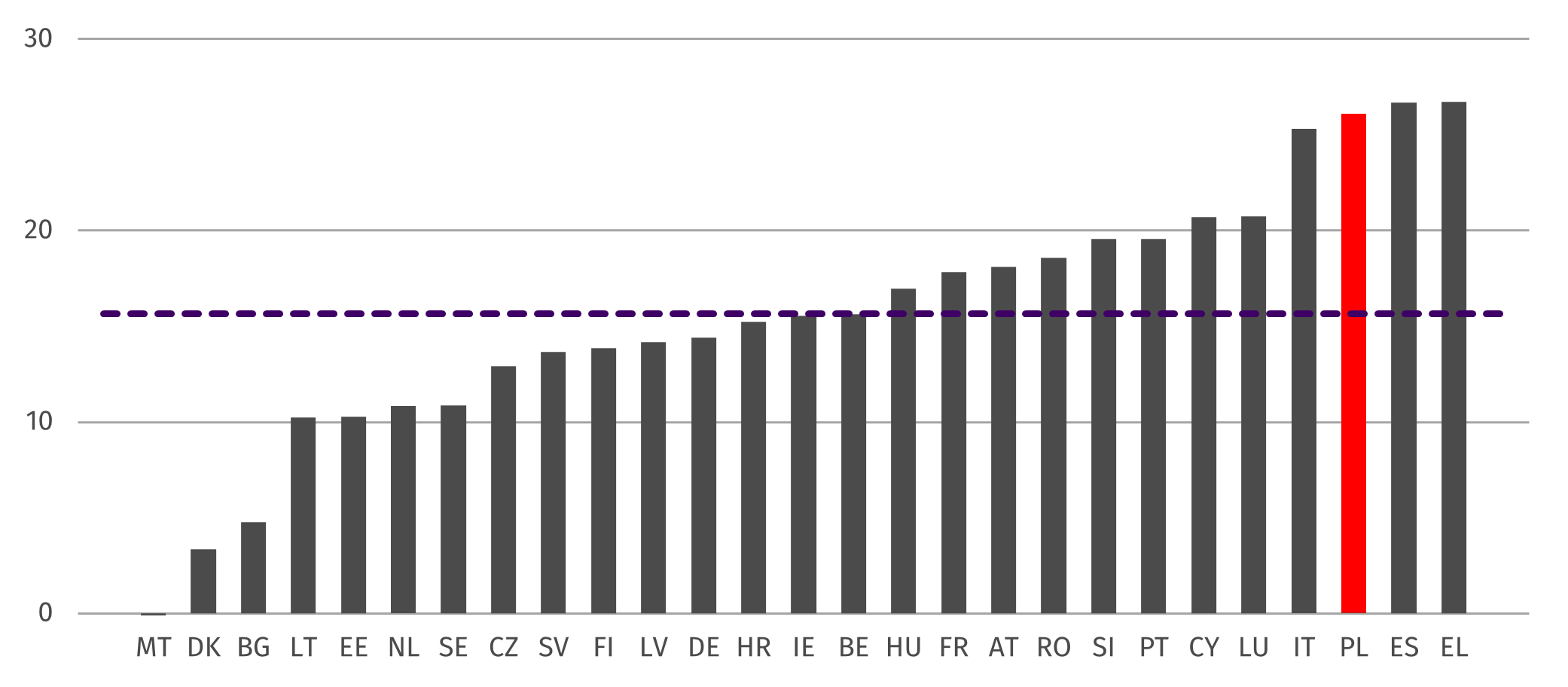

One of the key problems is the lack of system’s neutrality, which favors or penalizes selected industries or companies. The differentiation in VAT rates may serve as an example. In 2020, according to estimates of the Centre for Social and Economic Research, VAT revenues were over 26% lower than potential revenues due to the use of reduced rates and exemptions, while the average for the EU was 15.7%.

Figure 1. Lost VAT revenue as a result of applying reduced rates and exemptions as a percentage of potential revenue. Source: CASE

The text is based on the FOR Report: Evidence-based policymaking.

The full content of the publication can be found in the file to download below.

Contact do authors:

Marcin Zieliński, FOR President and Chief economist

[email protected]

Hubert Wejman, FOR Communication manager

[email protected]

Files to download